Today’s episode is hosted by Riva’s VP of Sales, Ken Lorenz. He will be talking with the Director of Product Management for Financial Services Cloud at Salesforce, Nirav Doctor; and they discuss the current state & future promises of customer data integration, what’s driving innovation at Salesforce Financial Services Cloud, and 3-year trends in Data, Customer360, and AI.

Guest: Nirav Doctor, Product Management for Financial Services Cloud

Nirav is passionate about delivering innovative solutions that transform customer, partner, and employee experience. As a product manager, he leverages his unique insights based on his extensive and diverse experience across consulting, customer success, and engineering roles. As an early member of the Financial Services Cloud team, he has been part of an internal startup at Salesforce, which has been one of the fastest-growing products in the history of Salesforce and has gone from 0 to $100+ M in a short span. Most recently, he has led the launch of the Corporate and Investment Banking solution, where he managed the complete product lifecycle from initial business case to market launch.

Subscribe and listen to the Rev-Tech Revolution podcast series on:

|

Spotify |

Apple Podcasts |

iHeart Radio |

Prefer reading over listening? We got you covered!

Introduction:

Welcome to the Rev-Tech Revolution Podcast, where we combine our 10 plus years of data integration experience and All-star guests to explore how organizations drive revenue through cutting-edge, Riva technology. Today’s episode is hosted by Riva’s VP of Sales, Ken Lorenz. He will be talking with the Director of Product Management for Financial Services Cloud at Salesforce, Nirav Doctor; and they discuss the current state & future promises of customer data integration, what’s driving innovation at Salesforce Financial Services Cloud, and 3-year trends in Data, Customer360, and AI.

Ken Lorenz:

Nirav, welcome. So great to have you on the podcast

Nirav Doctor:

Thank you so much Ken, it’s a pleasure to be here.

Ken Lorenz:

Well, fantastic. Well let’s so let’s dive right in. So, I’m sure everybody wants to know a little bit more about you. Who is Nirav and what, what are you passionate about? What gets you out of bed in the morning?

Nirav Doctor:

Yeah, such a great question. Right. What gets me out of, out of bed every morning is the

opportunity to transform the experience for customers, partners, and employees through innovative solutions. To that effect over the last 20 plus years, I’ve worked in a number of different enterprise software companies, both large and small, and, and, and in all of those roles, I’ve had the opportunity to work on transforming these customer experiences in one way or another.

So I started with some with a small start-ups developing web applications and then worked in large organization like Cisco and then got into the Salesforce ecosystem. And that has been such an amazing ride over the last 12 years with the first five years being a solutions architect, implementing all kinds of solutions using Salesforce products and partner products, and then I got into customer success at Salesforce. And, that is where I got to really see up close how the customers are adopting these solutions once they implement and how the users are adopting it – as well as how the technical teams update and maintain those solutions. And then, I got a fantastic opportunity to join the financial services cloud team at Salesforce on the product team about five years. And this is where we build industry vertical solutions for the financial services industry.

Ken Lorenz:

That’s fantastic. Nirav, it’s always a great pleasure to do work on things that you’re passionate about. I think it makes a real difference. So, for those that are not familiar with financial

services cloud, what is it? And why is it important?

Nirav Doctor:

That’s a great question too. Ken. Financial services cloud, as I mentioned, just started just

about six years ago. And the whole idea was that Salesforce has so many market-leading products for sales, marketing, service, automation, and analytics platform, and so many more.

However, those are all horizontal solution. So, what we found is that the customers take those best of breed solutions, but they tie those together and customize them for their own industry-specific use cases. I had a firsthand experience with those as a solutions architect in professional services, and I built a lot of those, including for financial services. And, and we saw that, you know, the time to market and the time to implement and the costs of implementing it can go down dramatically if more and more features are available through the product directly. So that was the guiding team with the financial services cloud, that if you were to build those industry vertical solutions and give the industry specific data, Business logic and UI, then, uh, we can take the customer 60, 70, 80% of the way there and the cost and the time to implement those solutions would go down dramatically. But not just that, you know, in my role in customer success the other thing I observed was that once a system integrator implements a solution and when they go away, the internal IT team now has to, you know, keep the lights on if you will, and keep maintaining that solution. And especially if there are a lot of customizations, they are harder to maintain and they can not focus on the innovations.

So, this is where if there are more features available right out of the box, then they don’t have to keep the lights on and they can focus on more innovations and how to drive maximum adoption through AI and other technologies. So that is the whole value proposition of FSC. And with that in mind, what we did is started building industry vertical solutions, starting with wealth management, and then we went on to deliver solutions for retail banking, commercial banking, insurance mortgage, and most recently, as you mentioned, we launched the solution for corporate and investment banking.

Ken Lorenz:

Excellent. So actually let’s, let’s take a little bit of a dive down there for a second. So are new release of, of CIB specifically it was addressing the needs for investment banks. Why, why should they specifically consider moving to the FSC?

Nirav Doctor:

Yeah. So when we talked to, uh, our investment banking customers and we talk about different flavors of those customers across four different continents and across different sizes. Whether

we talk to budget bracket or market or boutique investment banking firms, a lot of common teams emerge.

You know, the first thing from a business standpoint, what we learned is that this. Is really, really

dependent on relationships at the highest echelons of the organization, because you’re not sending some widget or just a piece of software. You are sending to the CEOs and boards of director. So you have to build and maintain those relationships. And then, uh, of course you are trying to maximize the deal mandates through those relationships and last but not the least, as you are going through that job, you need to make sure that you’re remaining compliant with all the relevant regulations, right. So we know that in financial services, regulations are omnipresent, but particularly with investment banking, there are a lot of relevant regulations that you absolutely must comply with.

So, we learned those themes and what we did is, within the financial services, we combined those industry insights with our expertise in the platform and the products to give a peeler solution for the corporate and investment banking vertical. And so we have industry specific data model, business, logic, and UI that can really transform the experience for the bankers and their end customers.

And so, so that reason, so that’s the key reason why the customers should really look at financial

services cloud. And so that will not only really accelerate that time to go live with that solution, but also ease the ongoing maintenance, and upgrades of got it.

Ken Lorenz:

Got it. Let’s move on to material non-public information. For the audience – can you define what it is and that comes into play in the banking world?

Nirav Doctor:

Yes, that is such a hot topic. I mentioned, I talked to 30 plus customers and I think for almost every one of them, that was the first thing that they mentioned to me. And they said that is such a hairy problem. And they literally said that, you know, if you don’t have a solution for that, we won’t sign the dotted line. Right. So it’s, it’s that important. And maybe from a banker standpoint, of course they want to remain compliant, but especially if you’re working on the compliance side of the house, they sweat this thing every single day.

So Material Non-Public Information really means when these investment banks, they are advising customers on sensitive deals, there is a lot of confidential information that they have, have access to. So let’s say the, a recent example of Salesforce, acquisition of slack, right? So what if the investment bank, a team that is advising Salesforce on net acquisition has that information that we are looking at acquiring slack and there, if the other, individuals within that bank, if they learn about that impending deal, they could potentially, engage in insider trading. Right. Which would be illegal and not only directly pre fines and filings, but a massive reputation in the industry too, for the bank.

So they want to make sure that they are preventing any such incident and if there is any audit, internal audit or a regulatory audit, they can demonstrate that only the people who are working on this deal and were pre-approved had access to any deal related information, or even the deal related call reports or any meetings that happen to discuss those things. This is where material non-public information becomes very important. Now, one thing to note over there is that a lot of these investment banks, they are not only providing these advisory services, but they are also providing these search and trading services in the global markets line of business, right, and they will be covering these same stocks like Salesforce and Slack. So it’s important that there are

some ethical walls in between the global markets and the investment banking sites of the house, and any material non-public information can never be accessed by the public while the deal is confidential. And sometimes even within the investment banking side, only the deal team should have, access to certain information. So that’s another place where that material non-public information needs to be, shared in a sensitive manner. And one important thing we learned through that process, that information may not reside only at the deal level, but sometimes just the knowledge that this particular meeting happened, but an executive could give a big hint. So, so a lot of times those events themselves are sensitive and they need to safeguard sharing of that information too.

Ken Lorenz:

And that’s why you, in the CIB product launch, you included the interactions module now is

a new set of functionality. To help separate the details of those meetings.

Nirav Doctor:

Exactly. What we learned from customers is – and our customers, some of them are really

creative – they started building some of the solution before we did. What they found is that, the

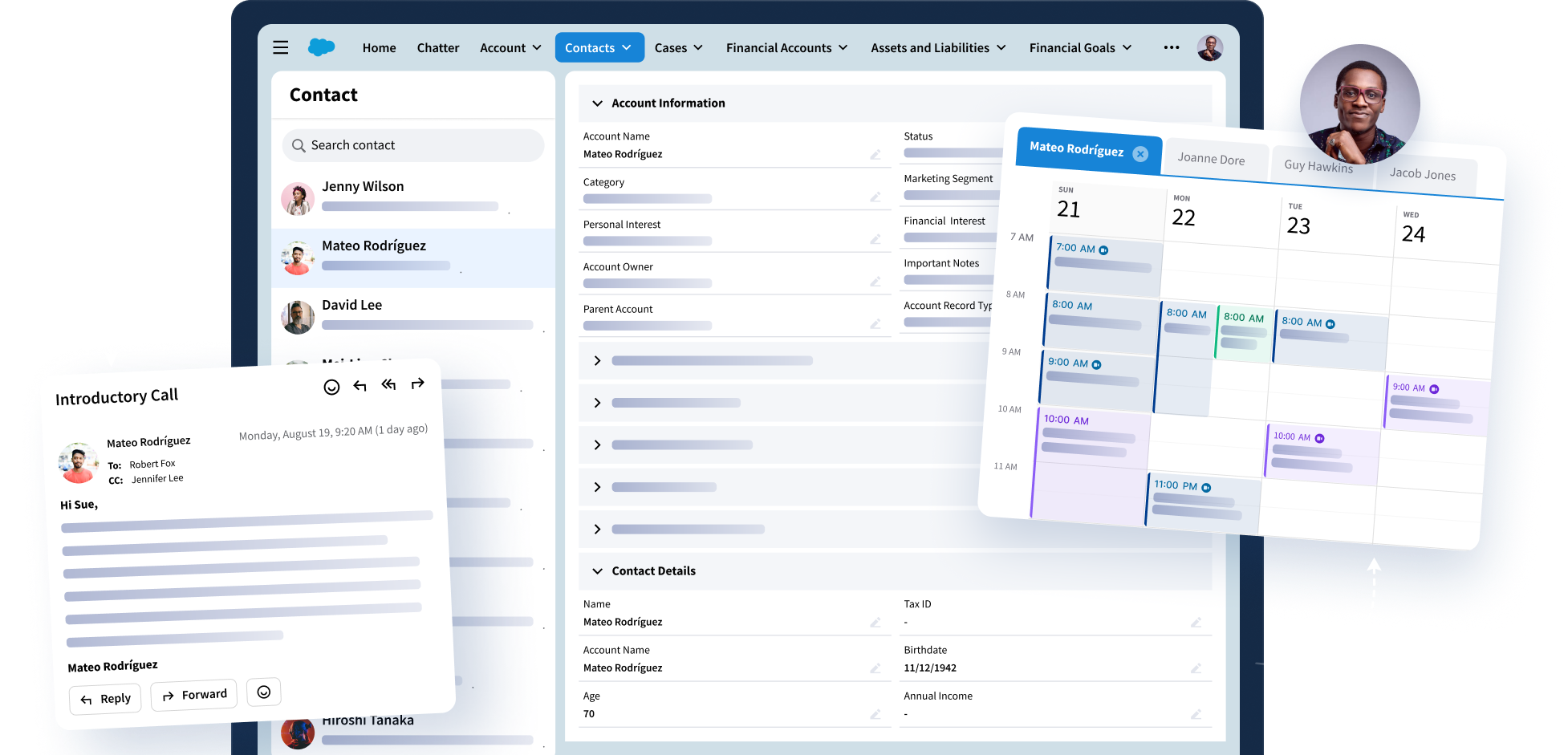

traditional, Salesforce activities, where they used to capture those events are captured. The call logs are, or the traditional opportunity, data model that Salesforce had was not suitable for really putting these types, you know, screws around the material non-public information. Sometimes it was, they found is a little bit too permissive and in more technical terms, you know, the activities would not have their own independent sharing and for opportunities, you could not turn off sharing viral hierarchy so anybody above you in the role hierarchy might be able to see that information and what we learned is a lot of times the team that they are, may have access to that information, but the management team may not see the sensitive information too. So, they were saying that we need to be able to turn off this role hierarchy-based sharing too. And what they were doing is they were building custom objects to model all these things and they were writing all the custom logic for the sharing. So what we did is we came up with a new data model for both managing the deals, as well as all the client meetings, as well as the call reports, and we came up with these interactions in the correction summaries data model, which has the full power of Salesforce platform sharing. However, it also gives us full control in terms of who you want to share that with. And on top of that, we build the compliant data sharing feature, which allows you as an admin or as a compliance team member to configure all those rules in terms of who gets access to any deal related information and what level of access they get, whether it’s read only, or read-write. So that’s the solution that we have built.

Ken Lorenz:

Well, I have to say thank you very much for letting us be part of that solution with you. Our

small role in that is to make sure that the calendar items and other customer data from Outlook gets synchronized properly to the interactions module. So we appreciate being part of that solution for you.

Nirav Doctor:

Absolutely.

Ken Lorenz:

When you think about the most forward-thinking banks – they need to solve for a 360 degree view of the customer – which Salesforce does so well. However, their end-users need to live in

outlook. What advice would you give a bank that’s trying to bridge that gap?

Nirav Doctor:

Yeah, so I want to start with a small story there. I was talking to, one of the managing directors at a leading bank. They came to the meeting and the first thing they said was “we had a breach”, because some of the sensitive call reports was shared via email by one of our bankers and it went to some people that should not have had this information. Now we are just trying to retrace this

thing, but we don’t even know if that email got forwarded and we don’t know exactly the whole chain of events and everything. We know that it happened, but we don’t even have a good way of understanding the scope of the damage and what we need to do to undo the damage.

So, so this is a tricky problem for the compliance teams, because while they want to make sure that they are remaining compliant, they don’t want to be slowing down the banking teams, you know, they are working very, very long hours working on the deal. They don’t want to compromise the ease of use. So this is where, what we found is that, it’s best to have an integrated solution. So we still let the bankers use Outlook to manage the calendar, manage all the events and everything. But when it comes to capturing the call reports and sharing them with the teams, whether it’s a deal team or coverage team as appropriate, we want to leverage the financial services cloud and make that experience as seamless as possible. We don’t want the bankers to have to re-enter all that meeting information and who attended and when the meeting was and whatnot. That is where an integration with outlook events become so critical. And that is where, you know, we really appreciate that Riva already integrates with the interaction summary and the interaction data model that we have built so that, you know, once a calendar event is synced to a within financial services cloud without re-entering any of that information, the banker can just go and quickly capture the call reports and share it with the deal team while remaining fully confident that as they are doing so they are not inadvertently sharing this information with somebody that should not have access to this. And this is also thanks to the

approval process that we have enabled on these entities, so that any new person that you are adding to the deal team or adding, to the call report itself, they can be pre-approved by compliance to receive that information. So you have full confidence, from the banker side, as well as compliance that you are not violating any rules related to sharing of MNPI.

Ken Lorenz:

That’s great, thank you. Now I’m going to ask you to put your revolutionary/visionary hat on

for a second. Tell us when you think is important in this space over the next three to five years. And I know you’re going to talk about customer 360 and AI, of course, but give us Nirav’s point of view here.

Nirav Doctor:

I think we have a great foundation with, getting a better understanding of who the client is and what the bank’s relationship with that client is and how they manage the deal life cycle and how they manage the client interactions and capture all the call reports, but there is so much more we

can do with this. Especially as we, we start bringing in more and more data into a financial services cloud. So that is one of the top things that we hear from our customers, that the bankers are not just living in Outlook and not just using financial services cloud, but they have to rely heavily on data from third party data sources, whether it’s PitchBook or you know, Cap IQ and other, or there are relationship databases also. So they are, and they are capturing or consuming news from other, sources like Definitive and Bloomberg. So they are still going to a lot of different systems. One of the key themes over the next few years that we see and which is also on our near term roadmap, is to integrate with those data sources and bring all of that information in one place in context of a particular client or in context of set up plans, which are part of your coverage. So it’s all filtered and sorted out for you so that you are not going to five or 10 different data sources, depending on how.

And one, uh, one of the key benefits of capturing all that information at the client level within the CRM system would be that, once you have that data, you can run analytics on that and AI to give a recommendation on the next best action, whether you know, this is the next client you should call, or this is the idea you should pitch to them. So you can start building those intelligence features on top of that. And you can also run all kinds of analytics in terms of, you know, who are the clients you want to target.

For example, this is the party who is most likely to transact with you, and that’s why you should pitch this deal to them. So these are the kind of integrations and intelligent business processes that you can start building on top of that. And then in another side of this equation is also to deepen the plan relationship by getting a better understanding of their interests, right?

So that is where, we are looking at building some features to track all the client interests. Like what are the kinds of things they are interested in? Are they interested in COVID or Brexit or specific pickers or, you know, so what are the key thing or they are interested in M&A. So we can start capturing all of those client interests in one place and also build plan lists to target based on those interests so that if you want to do a client outreach for a specific event or a specific deal shop or any given roadshow, then you can use those lists to do so. So the whole theme over here is get all the data in one place and start building those analytics and intelligent workflows on top of that and all in one place so it’s a single pane of glass for the banker and they have that full client 360 degree view in one place without doing the swivel chair across, you know, five or ten different systems.

Ken Lorenz:

Shifting gears a bit…We work across a number of different industries and we are seeing

titles like sales ops and revenue ops becoming more prevalent and having a real impact on the business. Are you seeing those titles or those titles showing up in financial services, and how did we develop a roadmap to address those new, new roles that are coming about?

Nirav Doctor:

So in terms of the titles – I think they are somewhat fluid, in their different titles. So within

the banks, they may call these by different names. But I think one of the key themes that we see is that – whatever you call them – Sales ops or revenue ops – they are looking for more and more

empowerment. What we hear from customers is they, and those people in those roles specifically is that for every small thing, they don’t want to depend on IT. They want to, uh, do some self-service if you will. And if they want to quickly go and run some audit report, or if they quickly want to run some report on the deal analysis or, you know, the win-loss analysis, what have you, they want that tools in the, at their fingertips, or even how similarly from a compliance angle, so as the sales ops or revenue is trying to make sure, uh, that they are remaining compliant with all this data sharing. So even there, they want to be able to manage the coverage team or the relationship teams, and then they want to do it on their own.

So we have tried to cater to those audiences by giving them a lot of configurable solutions so

that it’s not just that an IT admin, but when an end-user can go and configure those things and they don’t have to rely on developers, all the time.

Ken Lorenz:

Now we are ready to take some questions in from the audience. The first one is a curiosity about AI and, while I know you can’t share brand names, are there any FINS clients or stories that you

can talk about where we’ve had success with AI to date?

Nirav Doctor:

Yeah. So I think AI can have so many broad applications. One of the biggest themes that we have been working on, very actively is the relationship insights, you know, the Einstein relationship insights that, uh, you know, Salesforce has launched recently and, our CIB solution has already integrated with that so that the investment bankers can tap into that. Then to give you a very specific example in context of investment banking – so let’s say you want to pitch to a CEO and let’s take example of Benioff again, right? If you want to go and pitch to him, you can’t

exactly just cold call him. Right? So, wouldn’t it be nice if, you got a warm introduction through some mutual connections? And this is where you can leverage AI. You can, you know, try to figure out who connects me to Mark Benihof. And of course, there are structured data sources out there right now that some of our customers are already using and you are familiar with those. But when Einstein relationship insights is differentiated from those is, it goes and scours all the unstructured data on the web and social data and it uncovers those connections that you may not even be aware of. So it can go and figure it out that, oh, Ken here who works in my bank, sits on the board of this non-profit with the CEO, Mark Benihof so Ken might be able to introduce me to him. So, and this is something, this is a piece of information that does not set in any structured database, but spilled through scouring of the web, we uncovered this insight. So this is a great example of AI being applied.

There are some other examples which we don’t have yet, which we would hope to work towards is, you know, the wise technology and automatic transcription. And based on that, maybe giving an intelligence suggestion that, hey, based on your past interactions and this recent event in the market, you should reach out to this particular customer and pitch this particular idea. And then example could be, you know, being interest rates are low and they were trying to do a refinance or raise some capital. This is a good time to go and pitch this to them. So there are so many different use cases where you can start using AI.

Ken Lorenz:

Got it, got it. So I’m looking to see what additional questions we’ve got here. We’ve got one from Stephanie and she’s actually asking us to go back a little bit around why investment banks should consider FSC or why customers should consider FSC in general. Can you talk a little bit more about some of the verticalization that you envision coming forward and obviously we didn’t put a

forward-looking statement up, so we’ve got to be careful with that, but can you talk about that a little bit at a high level?

Nirav Doctor:

Yeah. And even with a given solution, I think we have pretty solid capabilities, right? So broadly I would classify those as, you know, data model, business logic, and custom UI, right. Built

specifically for investment. But, well, let’s talk about one specific example, right? So if we start talking about the whole MNPI data sharing, so that is one feature where some customers who are building those things custom, and what they have said is it took them anywhere from nine to 12

months, just to build that custom sharing logic along with the custom data model and no matter how you slice and dice the cost, like it’s, it could be running into millions of dollars just to implement that one feature.

Right. And we have a whole bundled suite of features like that. We have planned hierarchy to visualize that plan 360. We have, you know, the call reports that you can share, you know, with your team or coverage teams. And of course, to support all of that we have an investment banking-specific data model. And then we are obviously working on some of the other features that I mentioned related to analytics. So whether it’s related to your deal flow or whether it’s related to your win-loss analysis, or if you want to do some white space analysis. So there are so many areas of investment where we are still building a lot of different features. So I would say that anybody who starts with financial services cloud will certainly have a leg up in terms of the implementation cycle and even in terms of the user adoption, ultimately, so that they don’t have to build and maintain all of that custom code they can just go the last mile and to the final set of creeks, if you will, based on their unique business process.

Now one other thing which is also very beneficial if you think in terms of going with financial services cloud is a lot of our ISV partners are building to this new data model. Right. So, and Riva would be one example, right? So your outlook sync is already in integrated with our interactions and interactions summaries, or if somebody were to build a custom object for those same things, then they may have to build those integrations themselves. Right? So that’s just one example. But of course this data model is being used by other ISP partners to Google analytics and other deeper workloads, which complement what FSE already has. So, so you get to immediately take advantage of those ISV solutions also.

Ken Lorenz:

Excellent. So we’ve got another question and I think this one is actually for both of us from

Jagmet, he’s asking about when we talk about sharing items within calendar, how do we control this and ensure attachment and other items within the calendar can be controlled, plus is this user configurable? So I guess maybe I’ll, I’ll start half of that question and start on the outside of Salesforce and then I’ll pass it over to you on the inside of Salesforce. Yeah. So from, from a Riva perspective, you know, we’re, when we go to sync that particular calendar item, we, we’ve got a lot of choices on how we configure that. And there’s a number of business rules and flexibility that we can configure in to determine how that particular calendar item may be treated. Right. So as an example, we’ve recently added some functionality that allows a banker to specifically identify this meeting is going to be handled in a certain way when it gets synchronized. Synchronize all the detail, synchronize only the meeting itself, synchronize only portions of it, et cetera. So that the data that finds its way to Salesforce gets controlled by the configuration of the sync.

Now, I’m going to hand it off to you Nirav, once that once we’ve sent that data over to Salesforce, then, then how do you guys handle that and make sure that that only gets seen by the right people?

Nirav Doctor:

Absolutely. So what we do is, so this data gets sent into an NP call, us interaction and the related entity called interaction attendees. Like what we have done is created new web-based platform,

objects or BPOs as we call them internally. So these are brand new entities that we have created and they have all the power of Salesforce platform sharing features, but one key thing that we took care of, give the customers the ability to control whether they want to share those records by a role hierarchy or not. So you, so admins can configure whether they want to share these records with the people in the role hierarchy, or they don’t, they can simply turn it off.

So they have that one big lever of control that we have given. And the other thing that we have done is these entities have their independent sharing. So if you’re familiar with the activities, they they’re sharing follows the parent account or the parent contact with which they are associated. Not so with interactions and interaction summaries, you will have full control of who gets access to that so you can set the sharing model to private and then open up sharing as appropriate using all the sharing features.

Now, one of the thing that we have done is enabled approval processes on who gets access to this data. So we have the combined data sharing feature where you can add you know call the port participants or what we call is interaction participants and interaction summary participants, so for each of those records, you can individually add and remove people and assign them roles based on which they will get access. And if you don’t add them to that interaction or interaction summary as participants, they get no access whatsoever. But if you add them, then based on the centralized configuration, they get either read access or read-write access.

And also, as you are adding those people as a banker, you might still inadvertently add somebody from the public side or somebody who should not get access. So that is where the approval process comes into play. So that, you know, what we do is once that person is approved – if you have that turned on that approval process and once it is approved by the compliance based on any complete clearance, only then that person becomes active in context of that interaction or interaction summary, and only then the compliant leader sharing kicks off. So if you are using complaint data sharing in conjunction with this approval process, you have all the, uh, all the controls in place and it’s really airtight. So you have the full flexibility to share with whoever you want without, uh, you know, leaking that information to somebody who should not have that access.

Ken Lorenz:

Awesome. So there’s a follow-up here from Jagmet. He’s asking again, how is it auditable and integration reports can show the summary of who did what.

Nirav Doctor:

Yeah. So, that’s a big question. So. Right now we say we have a partial solution and there is another part of it that is on our roadmap that we hope to get to. So, in terms of the auditing for current access, if I talk about in the moment of time then we already have the share tables within Salesforce. We are using standard Salesforce share tables where these entries are in terms of who has access, what level of access they have. And, so on and so forth and what their role is.

So in the sharing visa and why, if something was shared with them. So we have those entries. So if you wanted to go and check a particular deal or a call report or an event and who had access to it and how, why they bought the access and what level of access, you can certainly go to that sharing table and see that. And we do have the UI and by the way, previous people won’t be available in classic, now it’s available in lightning too. So you can go and see it in the lightning experience. But yeah, finally, so it’s been there for a couple of years now, but the other aspect of this is the historical data, right? So if you want it to know that in the past, this pen was part of this building here, access to this is no longer part of the bank or the part of the deal team, and we no longer have that.

Now that piece we have not directly solved yet. That’s on our radar. However, if you know, the banks wanted to maintain that they do have the way to, you know, love whatever sharing had happened, so they can maintain a copy of that of the share table entries and, you know, keep it in, keep it up to date. So there is and interim way to do that. If you customize that one bit, and we do have some customers who have done that until we come up with that a solution for the historic data also.

Ken Lorenz:

So look maybe a little bit of a softball going in a little different direction. FSC for retail banking – how far has Salesforce gone? Are there any case studies that you can point to?

Nirav Doctor:

Okay. So the first step caveat, I know retail banking is not my domain. I’m not responsible. I may not have the best answer, but here are a couple of thoughts. And I know that on our website, we publish a lot of case studies and even ROI studies. So definitely check out the resources we have on the web. But if you are looking for something more specific, you can follow up with me offline and I can connect you to the right marketing people who can provide more details.

Ken Lorenz:

That’s great. So I’m running out of questions that have been asked here. If anybody has any

additional questions, make sure you add them to the questions and answers. Betsy, I’m going to ask you to chime back in as well. Do you have any other questions that have come in any other way?

Betsy Peters:

Nope. I think you got most of it, gentlemen, you’re doing a terrific job and thanks to everyone in the audience who’s participating so nicely we appreciate it. It helps us direct where to go next, obviously. So we certainly have time for one or two more. If anyone has any questions. If not, we can have them talk about the holy Roman empire, who I was neither.

Ken Lorenz:

Well, if we don’t get any additional questions, Nirav, I’m going to give you 20 questions in

60 seconds.

Betsy Peters:

All right, we’ll give it another minute or so.

Ken Lorenz:

Alright. Are you game for a couple of rapid-fire questions while we’re waiting Nirav? Coffee

or tea?

Nirav Doctor:

Tea

Ken Lorenz:

Mac or PC?

Nirav Doctor:

Mac

Ken Lorenz:

I love it. Red or blue?

Nirav Doctor:

Blue

Ken Lorenz:

Skiing or beach?

Nirav Doctor:

Beach.

Betsy Peters:

Dog or cat?

Ken Lorenz:

Ahh, good one.

Nirav Doctor:

Dog

Betsy Peters:

All right. Well, I am not seeing any other questions from the audience, so we can bring this to a close. Thank you both very much for an interesting conversation, and especially to you Nirav for

your time and your insights. Thanks to everyone on the call for your questions and your attention.

And as we’ve now officially recruited you into the Revolution, we want you to know about our next conversation – with best-selling author Tony Hughes, where we’ll talk about his new book Tech Powered Sales. We’ll send you an invite for October 12th, so you can learn about how customer data powers sales cyborg success. So with that, thank you very much again, and we hope you have a terrific week.

Ken Lorenz:

Thank you very much.

Nirav Doctor:

Thank you very much. Thanks for the opportunity.